By Marilyn Carr

Sponsored by Ingram Micro and Microsoft, this paper is part of a series developed by IDC to educate organizations on the cloud

provide guidance on how to succeed in the cloud marketplace.

Cloud and the 3rd Platform of Computing

In 2008, IDC started to notice the IT industry was at the beginning of a hyper-disruption – one of

those massive shifts that comes along every 20–25 years. In 2011, we had seen enough to give it a

name: the 3rd Platform. The new era of technology is built on the four technology pillars for

innovation and growth: cloud, mobile, big data, and social technologies (see Figure 1).

Of these four pillars, cloud perhaps represents the biggest disruption. That's because it changes

the way companies consume and pay for access to technology. But more and more these days,

companies are realizing that, beyond a better way to consume software, the cloud offers them

brand-new ways to solve their business problems. Simply consider some of the file synchronization

services that allow someone to see his/her files on any device, anywhere. New capabilities like this

and others are unleashing the imaginations of companies across the globe, tackling business

problems with the cloud that were previously unsolvable.

This IDC Market Spotlight begins with definitions of cloud and its various forms and then goes on to

outline the vast and growing adoption of cloud technologies. If you want a better understanding of

what cloud is and how fast it's growing, please read on.

The Era of the 3rd Platform

What Do We Mean by Cloud?

A lot of people have a general understanding of what the cloud is. But they get confused once they dive into the details. Let's first have a look at the different flavors of cloud, which will help clarify the various options available.

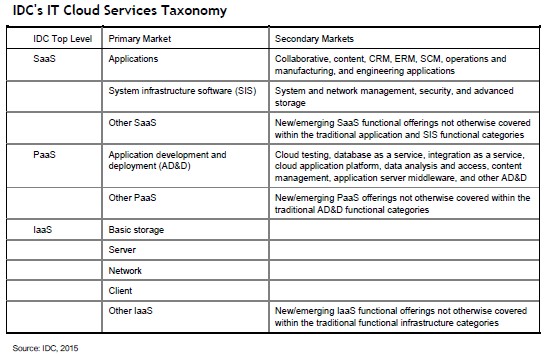

IDC's IT cloud services taxonomy is based on the widely used U.S. National Institute of Standards and Technology cloud services categories: infrastructure as a service (IaaS), platform as a service (PaaS), and software as a service (SaaS) (see Table 1).

IDC's IT Cloud Services Taxonomy

The cloud market is highly diverse. At the highest level, the two types of deployment models for cloud services are public and private:

- Public cloud services are shared among unrelated enterprises and consumers; open to a largely unrestricted universe of potential users; and designed for a market, not a single enterprise.

- Private cloud services are shared within a single enterprise or an extended enterprise, with restrictions on access and level of resource dedication and defined/controlled by the enterprise (and beyond the control available in public cloud offerings). Private cloud services can be onsite or offsite and can be managed by a third party or in-house staff. A self-run private cloud is a cloud service that an enterprise owns and operates itself. The enterprise may have acquired the hardware and software components required to build a private cloud and assembled it (or had a systems integrator do so). A managed private cloud is an enterprise-owned cloud service that is operated by a third-party services firm. This is a less common model and parallels traditional onsite managed services arrangements in which the customer uses third-party staff to operate its traditional on-premise IT environment.

- A virtual private cloud (VPC) service is a premium version of a public cloud service, with tiered options for greater privacy/security and customer control. Physical resources are not dedicated to a single customer — allowing the service provider and the customer to benefit from public cloud economics.

- A dedicated private cloud (DPC) service is provided on dedicated/isolated physical resources to a single enterprise or an extended enterprise.

Two other often-discussed cloud services deployment model terms are hybrid cloud and community cloud:

- Hybrid cloud: The term hybrid cloud is used to describe the consolidated coordination/management of multiple cloud services. Hybrid cloud services include "public/public," "public/private," and "private/private" combinations. IDC does not classify collaborations between cloud services and non-as-a-service IT as hybrid cloud services.

- Community cloud: A "community cloud" is a multi-enterprise cloud service that's been commissioned by, and is controlled by, a group of enterprises that have shared needs, control/specify the functionality of the services, and share the cost burden.

The cloud services deployment variables include:

- Where the cloud service is located (on the customer's site or at a third-party service provider)

- Whether the cloud service is consumed as a shared or a dedicated service (public versus private)

- The type of provisioning (completely dedicated, completely shared, or private cloud provisioned from the public cloud shared resource pool)

- The management options, which may include both internal IT and external service providers

Consideration of all the aforementioned variables means there are several pros and cons to weigh before deciding what shape your cloud solution will take, and the context of the variables will likely change over time. That's why it is important to create a road map for incorporating cloud into your technology portfolio, something that is best developed in consultation with a cloud subject matter expert.

IDC also describes cloud services through the key attributes that an offering must manifest to end users of the service (see Figure 3). Cloud services require support of all of these attributes. This checklist of attributes can be used when evaluating cloud offerings from potential service providers to ensure that you are actually getting what you think you are getting.

Current Cloud Adoption and Projected Growth

Cloud is an essential part of the much broader, and bigger, impact of the shift in IT and its applications. Big data, mobile, and social technology solutions are all heavily dependent on the cloud services delivery model. In effect, these solutions can't exist without the cloud model as the underlying platform. In turn, cloud services growth is highly dependent on the other three 3rd Platform technologies. Look for growth of cloud services to be positively impacted by breakthroughs in mobile, big data, and social technologies and solutions starting this year and beyond. Conversely, major breakthroughs in these areas will require (and drive) major investments in cloud technologies and services.

We now are entering what IDC calls the "innovation stage" of the "3rd Platform" (and cloud) marketplace — in which we predict that a tripling community of developers will create a 10-fold increase in the number of new killer cloud-based solutions in the next four to five years. Many of these "killer apps" will be innovative and disruptive industry-focused solutions, created and marketed on industry-specific cloud services platforms and marketplaces, run by leaders in each industry seeking to attract communities of thousands of innovators to create valuable new services. Line-of-business executives will drive many of these cloud investments as cloud services become much more valuable and strategic to enterprises. This is very good news for those adopting cloud solutions because it means they will continue to benefit from innovations that will spur productivity and strategic advantage, enhancing the return on investment.

The "greater cloud market," including cloud services and all the hardware, software, and services enabling cloud services, will hit $118 billion in 2015 and grow to over $200 billion by 2018. Public IT cloud services spending, a major part of the greater cloud market, accounted for $56.6 billion in 2014 and will reach over $127 billion in 2018 at a compound annual growth rate (CAGR) of 22.8%, or about six times the rate of overall IT market growth.

In 2018, public IT cloud services will drive nearly 20% of the $640 billion aggregate spending in applications, development and deployment tools, infrastructure software, storage, and servers. Collectively, public IT cloud services will account for 55% of spending growth. Clearly, cloud is a very significant part of how companies are consuming technology today.

SaaS, which accounted for 70% of 2014 cloud services spending, will continue to dominate public IT cloud services spending, as most customer demand is, understandably, at the application level. PaaS and cloud storage services will be the fastest-growing IT cloud services categories, driven by major upticks in developer cloud services adoption and big data–driven solutions. IaaS will remain the second-largest IT cloud services category — boosted largely by cloud storage's 31% CAGR from 2014 to 2018 — even as intense price competition and looming consolidation pressure IaaS price points.

North America accounted for 68.1% of IT cloud services spending in 2014, but that share will drop to 61.6% by 2018. In Europe, the second-largest region, share will rise from 20.7% in 2014 to 24.2% in 2018 (see Figure 4).

Essential Guidance

Cloud is a substantial transformative force impacting all areas of IT supply, composition, and consumption for all buyers and sellers. IT buyers are shifting steadily toward cloud-also and cloud-first strategies. In fact, IDC predicts that 70% of CIOs will adopt a cloud-first approach by 2016. Nearly all are reconsidering their IT best practices to embrace hybrid cloud construction and operations, secure data management, end-to-end governance, updated IT skills, improved multivendor sourcing, and a host of other key topics. The ballooning of supply — a huge increase in the number and diversity of cloud services available — is leading to vastly increasing customer demand as IT decision makers look well beyond automation (IT's traditional realm) and into new possibilities for data management, customer and employee engagement, application development and testing, and a range of other net-new possibilities. Smart IT leaders will focus on this guidance.

The cloud has changed the fundamental nature of computing and how business gets done, and it will continue to do so through 2020. In fact, IDC predicts that, by 2020, clouds will stop being referred to as "public" and "private," and ultimately they will stop being called clouds altogether. It is simply the new way business is done and IT is provisioned.